Foreclosures can look like incredible deals. A house that might normally sell for $300,000 suddenly pops up for $200,000 and buyers feel like they’ve found a hidden opportunity.

But here’s the real talk: that discount often comes with hidden costs that many buyers don’t see until it’s too late.

I’ve personally seen buyers get excited about a $200K foreclosure and end up spending $80K or more in repairs and legal cleanup before the property was even livable.

If you’re thinking about buying a foreclosure, here are four areas where unexpected costs usually show up.

1. Inspection Problems: You’re Often Buying Blind

Many foreclosure purchases—especially auctions—are “as-is” and sight unseen.

That means:

- No professional home inspection

- No seller disclosures

- No repair negotiations

Even when inspections are allowed (like with bank-owned REO properties), utilities are often turned off. Without electricity or water, inspectors can’t fully test:

- HVAC systems

- Plumbing pressure

- Appliances

- Electrical panels

That also makes it harder to detect mold, water damage, or hidden plumbing issues.

So the property that “looks fine” during a quick walkthrough may have serious problems hiding behind the walls.

2. Title Problems: The Surprise Debts

A foreclosure sale doesn’t always wipe out every debt attached to a property.

Without a proper title search, buyers can inherit issues like:

- IRS tax liens

- Mechanic’s liens from contractors

- Judgment liens

- Unpaid utility balances

There’s another common trap with HOA foreclosures.

Sometimes buyers win a property at an HOA auction for a cheap price, only to discover the original first mortgage still exists. Imagine paying $40,000 at auction and then learning there’s still a $200,000 mortgage attached to the property.

This happens more often than people think.

In some cases, the previous owner or the IRS can even exercise a right of redemption, meaning they can reclaim the property after the sale by repaying the auction price plus interest.

If that happens, any repairs you started may become a sunk cost.

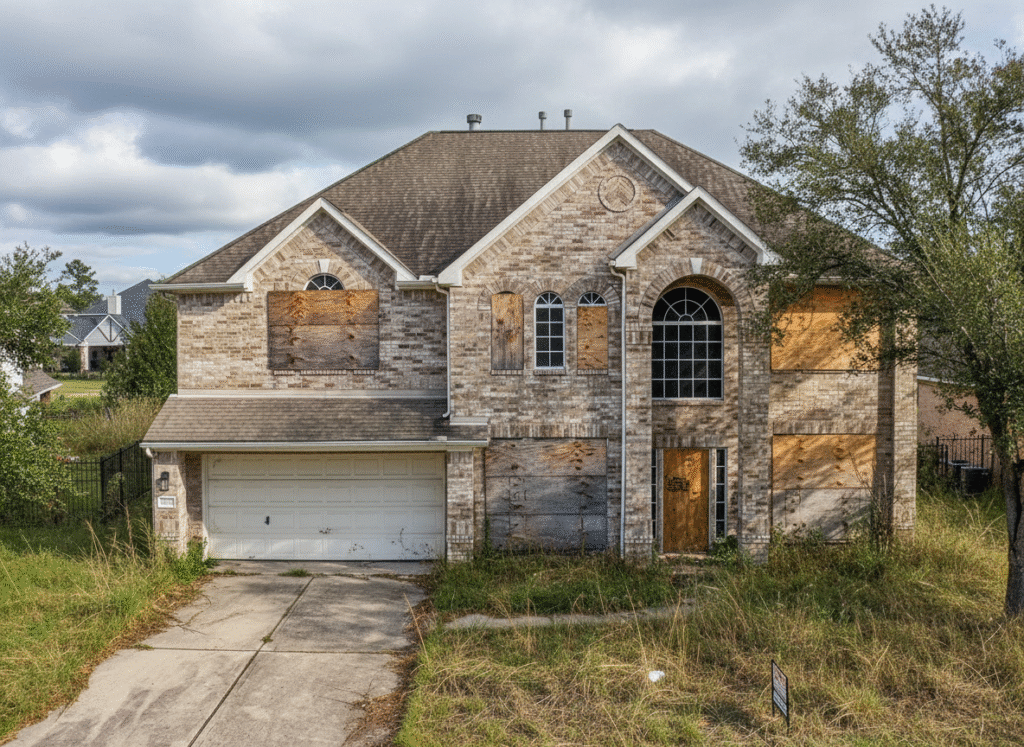

3. Repair Costs: The Real Budget Killer

Distressed properties often come with years of deferred maintenance.

Sometimes the damage is worse.

Vacant homes are targets for vandalism and theft. I’ve walked into foreclosures where thieves had removed:

- Copper plumbing

- Electrical wiring

- Appliances

- HVAC components

- Light fixtures

Replacing these systems can cost $5,000–$15,000 or more.

Other common issues include:

- Mold from lack of climate control

- Burst pipes after improper winterization

- Roofs and HVAC systems that were ignored for years

Even experienced investors usually add 15–20% contingency to their repair budgets because surprises are so common.

4. Financing Challenges

Another shock for many buyers is how hard it is to finance foreclosures.

At foreclosure auctions, traditional mortgages are usually not allowed. Buyers must often pay:

- Cash

- Certified funds

- Within 24–48 hours of winning the bid

Even with bank-owned properties, lenders may hesitate if the home is in poor condition.

Appraisers may flag issues like:

- Peeling paint

- Missing railings

- Structural concerns

These problems must often be fixed before the lender will approve the loan.

Because of these hurdles, many investors rely on hard money loans, which come with:

- Interest rates of 10–15%

- Short repayment timelines (6–24 months)

- Down payments of 20–30%

And on top of that, buyers using financing are competing with experienced cash investors who can close quickly.

The Bottom Line

Foreclosures can still be great opportunities.

But the biggest mistake buyers make is focusing only on the purchase price instead of the total cost of ownership.

Between hidden repairs, title issues, and financing hurdles, that “cheap deal” can become expensive fast.

The good news? Most of these risks can be spotted before you buy—if you know where to look.

Need Help Analyzing a Foreclosure?

If you’re considering a specific foreclosure, I’m happy to take a look and help you spot potential red flags before you commit.

Want me to analyze a property for hidden risks?

Book a quick call here: https://calendly.com/brunofineproperties/30min

A 15-minute review could save you tens of thousands of dollars.